“Over the years we’ve invested significantly in our field data team - focusing on producing trusted ratings. While this ensures the accuracy of our Ratings, it doesn’t allow the scale across the thousands of projects that buyers are considering.”

For more information on carbon credit procurement trends, read our "Key Takeaways for 2025" article. We share five, data-backed tips to improve your procurement strategy.

One more thing: Connect to Supply customers also get access to the rest of Sylvera's tools. That means you can easily see project ratings and evaluate an individual project's strengths, procure quality carbon credits, and even monitor project activity (particularly if you’ve invested at the pre-issuance stage.)

Book a free demo of Sylvera to see our platform's procurement and reporting features in action.

Why The (Corporate Sustainability Reporting Directive) CSRD Timeline Is Causing Confusion

Since its adoption,the Corporate Sustainability Reporting Directive has been positioned as a clear step change in sustainability reporting. For teams inside large organisations, however, the challenge has never been understanding why CSRD exists — it has been working out what applies when across complex group structures.

Most large enterprises already know that CSRD expands reporting scope, depth and assurance well beyond the Non-Financial Reporting Directive. What creates friction is translating the evolving CSRD timeline into concrete decisions: which entities are in scope, which reporting year applies, and how EU and non-EU operations fit together within a single reporting process.

In practice, this leaves many teams in an uncomfortable position. They are expected to prepare data, systems and governance, while national transposition, scope changes and EU-level delays continue to shift timelines. The question is no longer whether CSRD applies, but how to plan responsibly when obligations are staggered and clarity arrives late.

What Has (And Hasn’t) Changed In The CSRD Timeline

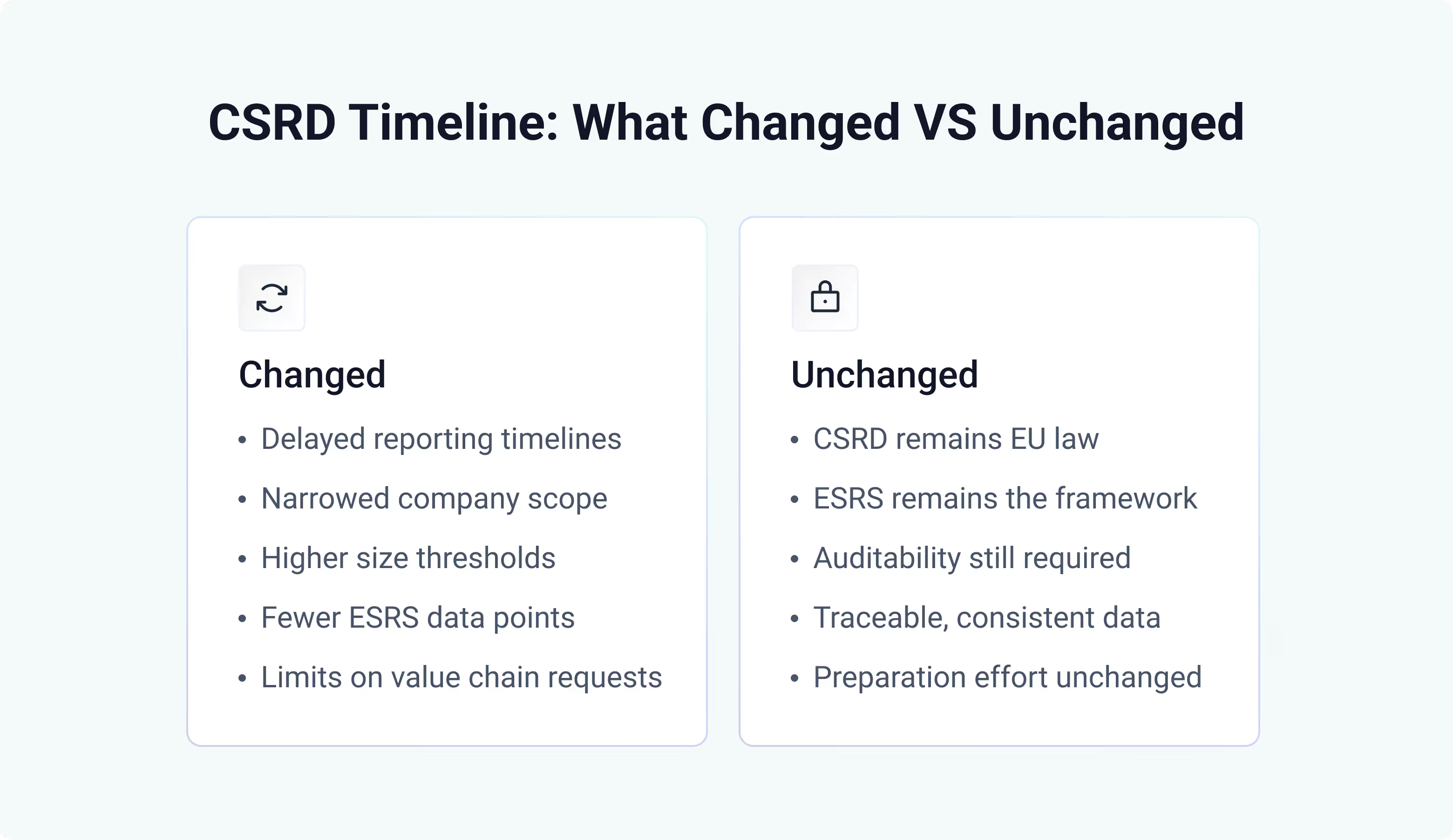

Since 2024, the EU has adjusted both the timing and the scope of CSRD, while leaving its core objectives intact. The reporting timeline remains phased by company size and type, but the EU has formally delayed first reporting for companies that would otherwise have reported for FY2025 or FY2026. In parallel, EU institutions reached an omnibus agreement in late 2025 to substantially narrow the scope of CSRD, refocusing mandatory reporting on the largest companies. Under the agreed direction of travel, thresholds are raised to around 1,000 employees and high turnover levels, significantly reducing the number of companies expected to fall within scope once the amendments are fully adopted.

The same package aims to simplify how CSRD is applied in practice. Planned changes include a material reduction in ESRS data points, a clearer focus on information that is material for fair presentation, and safeguards for smaller companies in the value chain, limiting the extent of data requests they can be subjected to.

What has not changed is the framework for companies that remain in scope. CSRD continues to apply under EU law, reporting is anchored in ESRS, and sustainability information is expected to be auditable, traceable, and consistent year over year. The scope may be narrower and timelines longer, but for obligated companies the level of preparation required has not diminished.

In other words, the CSRD compliance timeline may feel longer on paper, but the preparation workload has not shrunk.

The CSRD Directive Timeline In Context

To understand the current CSRD timeline EU companies are facing, it helps to place it alongside earlier regulation.

The Non-Financial Reporting Directive applied to a relatively small group of large public-interest entities and allowed significant flexibility in how non-financial information was disclosed. CSRD replaces this approach with a more standardised and prescriptive framework built around the European Sustainability Reporting Standards.

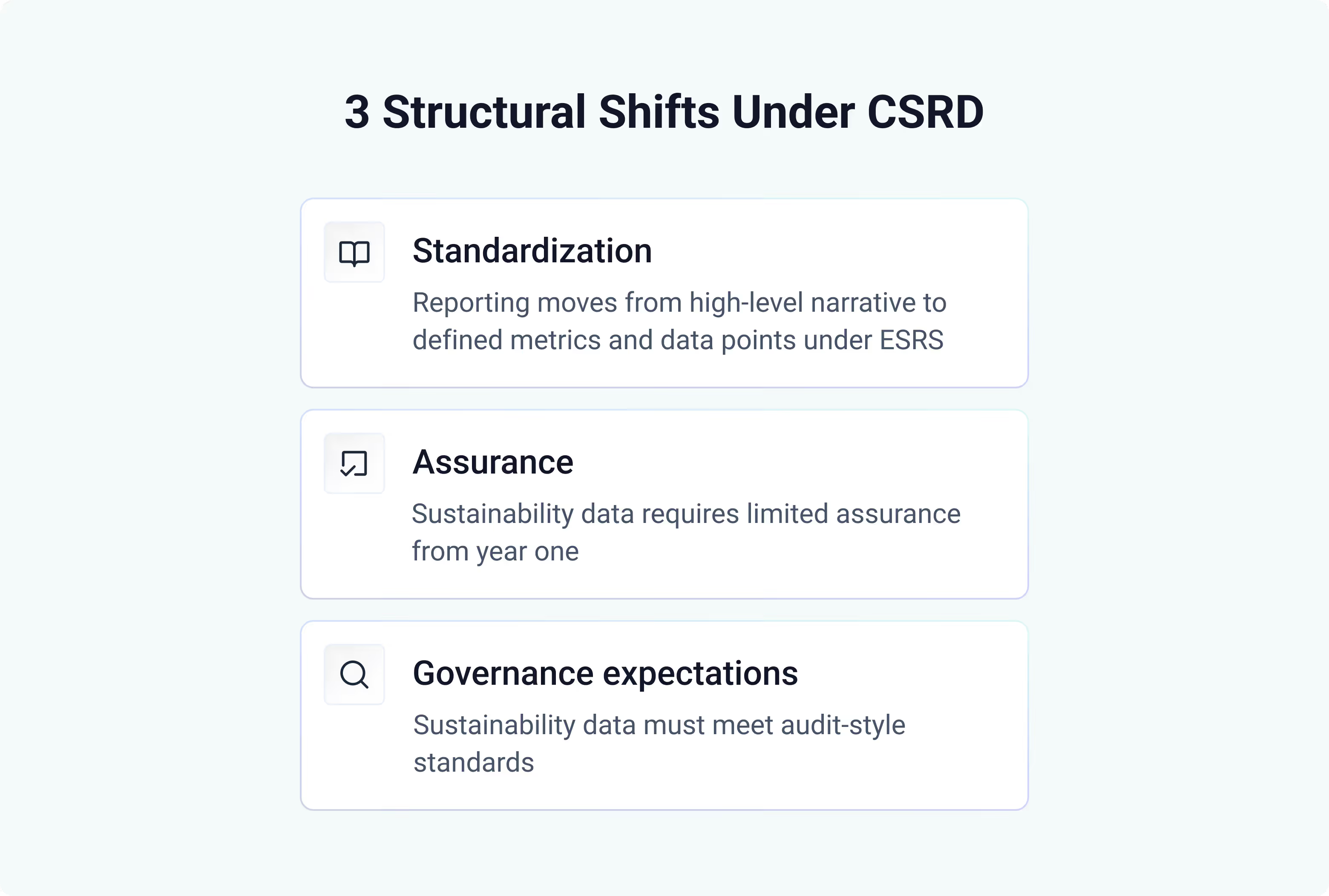

The CSRD timeline reflects three structural shifts compared to NFRD:

- Standardization: reporting moves from high-level narrative to defined metrics and data points under ESRS.

- Assurance: sustainability information becomes subject to external limited assurance from the first reporting year.

- Governance expectations: sustainability data is expected to meet audit-style requirements for consistency, traceability, and internal control.

While recent EU decisions have narrowed the group of companies ultimately required to report and extended timelines for some, these shifts explain why expectations for data quality and reporting discipline remain high for companies that fall within scope.

CSRD Reporting Timeline By Company Type

Phase 1: Companies Already Under NFRD

This group is unchanged and already in motion.

These are EU public-interest entities that were already subject to the Non-Financial Reporting Directive. In practice, this mainly includes listed companies, banks and insurers operating in EU regulated markets.

For these organisations, the CSRD timeline has not shifted. Reporting applies to the 2024 financial year, with first CSRD-aligned reports published in 2025. These companies are not affected by the stop-the-clock delay or the omnibus scope adjustments and are expected to be well advanced in implementation.

For many, the challenge is no longer whether CSRD applies, but whether underlying non-financial data is ready for assurance.

Phase 2: Other Large EU Companies

This is where the most significant change to the CSRD timeline has occurred.

Under the direction of the omnibus agreement, CSRD now applies to a narrower group of large EU companies. The revised scope focuses on organisations that meet both of the following thresholds:

- More than 1,000 employees

- Net turnover above €450 million

These companies were originally expected to begin reporting based on the 2025 financial year. Under the stop-the-clock mechanism, this has been delayed by two years.

The earliest reporting year for this group is now the 2027 financial year, with first CSRD reports published in 2028.

While this delay reduces the number of companies immediately in scope, it does not reduce the complexity of reporting. Many organisations in this group have never produced structured non-financial reporting at scale and underestimate the effort required to prepare auditable data across sites, suppliers and value chains.

Phase 3: Listed SMEs

Listed SMEs were originally included in the CSRD phase-in timeline, but this has materially changed.

Under the current political direction of the omnibus agreement, listed SMEs are expected to be removed from mandatory CSRD scope altogether, subject to final legislative adoption. Transitional opt-outs are no longer the main story; the direction of travel is exclusion rather than delayed inclusion.

In practice, this does not mean reporting pressure disappears. Listed SMEs may still face indirect requirements through value-chain data requests from larger customers and financial institutions. However, new value-chain caps explicitly limit how far those requests can extend.

For SMEs, the CSRD timeline has shifted from direct obligation to indirect influence.

Phase 4: Non-EU Companies

The CSRD timeline for non-EU companies remains largely intact.

CSRD applies to non-EU groups that generate more than €150 million in net turnover within the EU and have either a large or listed EU subsidiary, or a significant EU branch.

For these organisations, reporting applies to the 2028 financial year, with first CSRD reports published in 2029. This phase has not been materially changed by the stop-the-clock delay.

This remains one of the most underestimated elements of CSRD adoption. Many non-EU parent companies continue to view CSRD as a regional issue until EU customers, regulators or financial partners begin requesting aligned sustainability information.

The CSRD Assurance Timeline: What To Expect

Another area where the CSRD assurance timeline causes uncertainty is the move from limited to reasonable assurance.

Initially, CSRD requires limited assurance on sustainability reporting. Over time, the EU intends to move towards reasonable assurance, bringing sustainability reporting closer to financial audit standards.

This has two implications:

- Data collection and controls must be designed with assurance in mind from the start.

- Manual, spreadsheet-based reporting processes become increasingly risky.

Companies that delay investment in structured data collection often find themselves redesigning systems later at higher cost.

Why CSRD Delays Don’t Reduce The Preparation Burden

A common reaction to EU-level delays is to treat them as breathing room. In practice, CSRD implementation timelines are dominated by internal complexity rather than external deadlines.

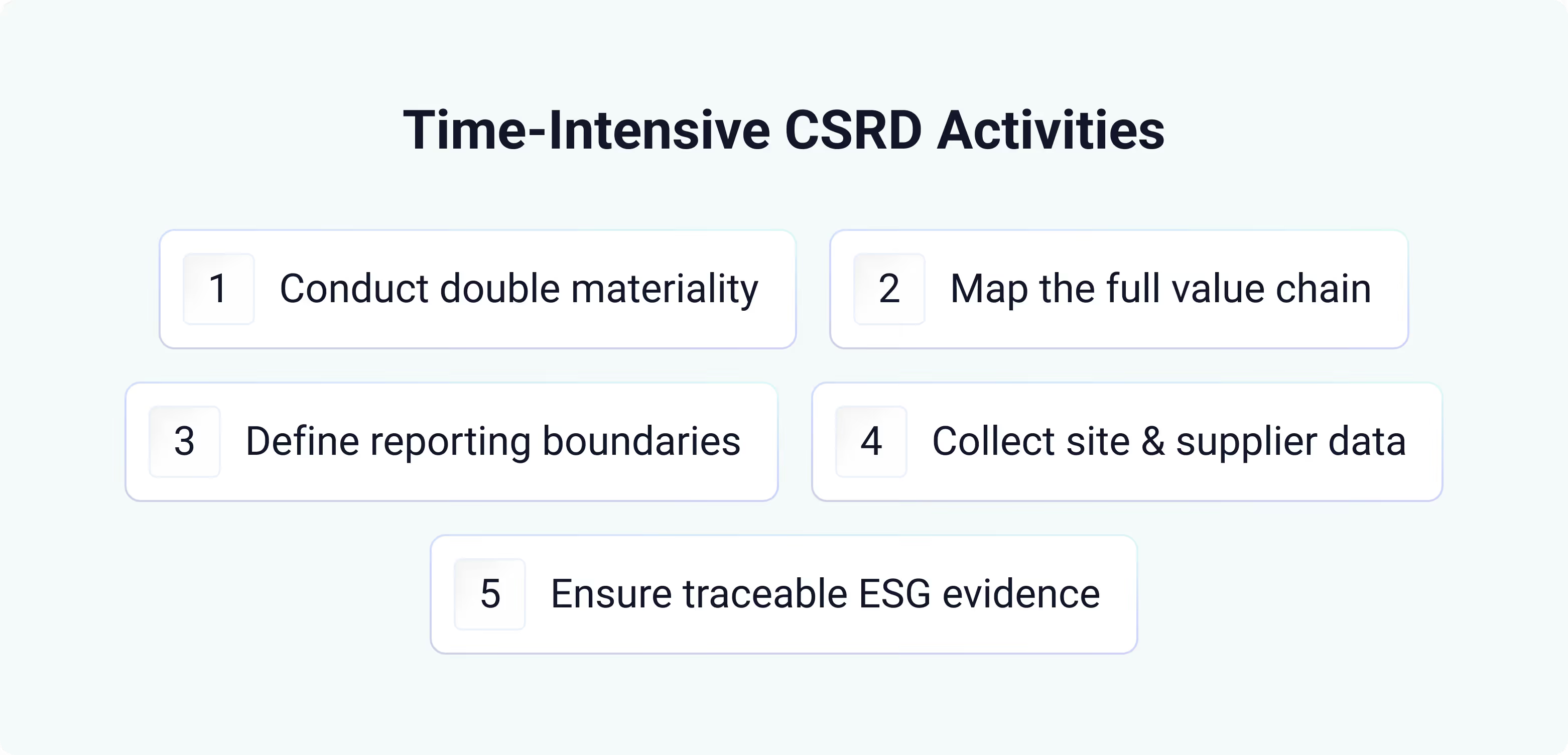

Key activities that take time regardless of reporting year include:

- Performing a double materiality assessment

- Mapping the entire value chain

- Defining consistent reporting boundaries

- Collecting non-financial information across sites and suppliers

- Establishing traceability and evidence for ESG data

These activities are particularly demanding for waste, materials and circular economy data, which often sit outside core financial systems.

Delays do not simplify this work. They merely shift when its absence becomes visible.

What The CSRD Timeline Means For Data And Corporate Sustainability

The CSRD reporting requirements timeline makes one thing clear: sustainability reporting is no longer a standalone exercise. It is becoming part of the standard reporting process, governed by the same expectations around accuracy, consistency and auditability.

For many organisations, the weakest point is non-financial data. Waste quantities, treatment routes, supplier information and environmental impacts are often scattered across invoices, contractor portals and local systems.

Without early investment in data collection and standardisation, reporting teams face last-minute consolidation exercises that undermine both accuracy and credibility.

How To Use The CSRD Timeline Strategically

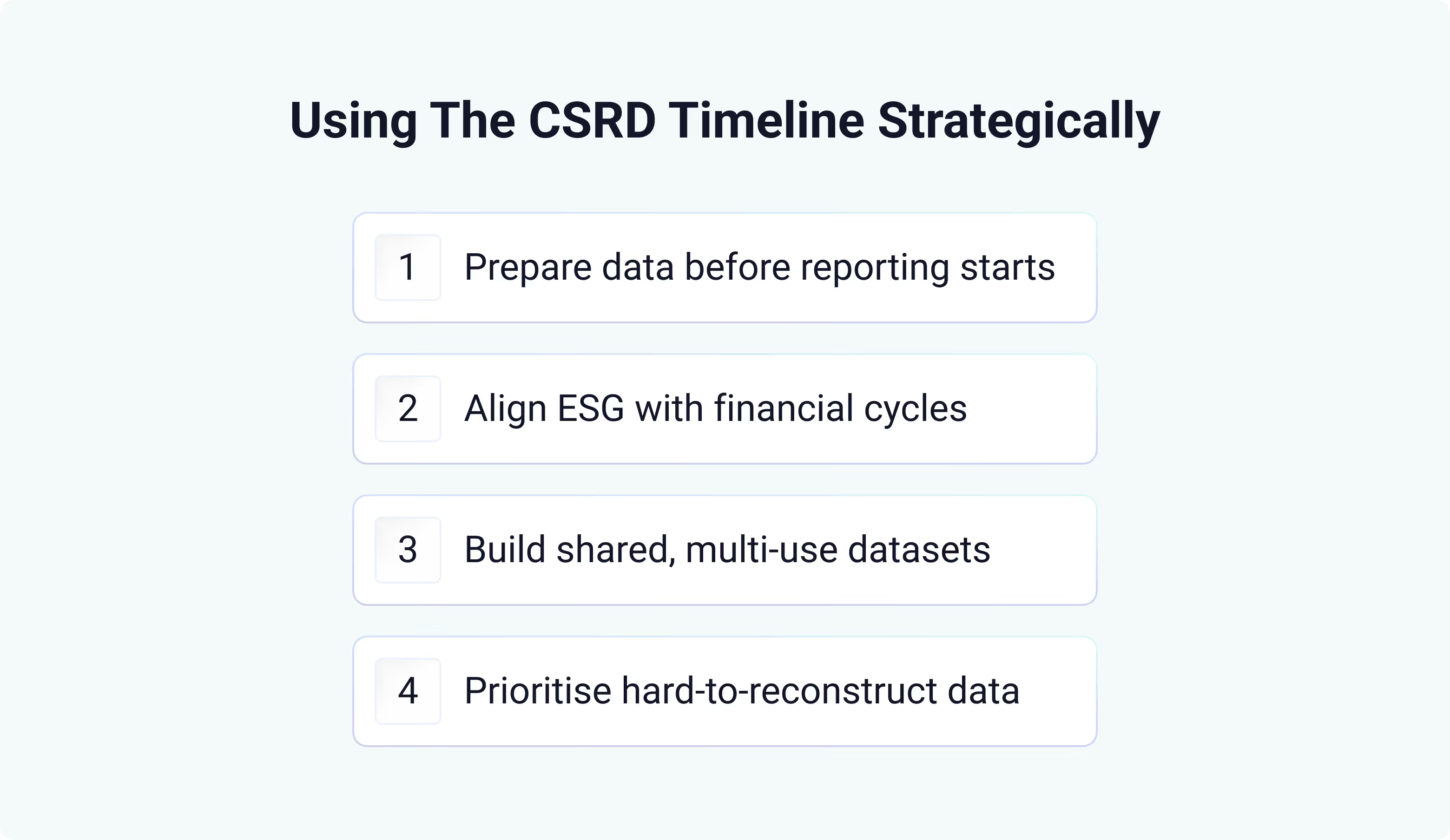

Rather than asking “when do we have to report?”, more mature organisations are asking “what needs to be ready before we report?”.

Using the CSRD implementation timeline effectively means:

- Treating earlier phases as learning periods, even if your entity reports later

- Aligning sustainability reporting timelines with financial year cycles

- Building shared datasets that serve compliance, performance management and decision-making

- Prioritising areas where data is hardest to reconstruct retroactively

This approach reduces risk and avoids the trap of treating CSRD as a one-off compliance project.

Where geoFluxus Fits Into CSRD Readiness

For organisations managing complex waste streams, CSRD readiness depends heavily on non-financial data quality.

geoFluxus supports CSRD reporting by structuring waste, materials and circularity data in a way that aligns with European Sustainability Reporting Standards. Data is standardised across sites and vendors, linked to source documents and made available for both reporting and analysis.

This allows teams to respond to CSRD reporting requirements without rebuilding datasets every reporting cycle, and to support assurance processes with traceable evidence.

If you want to see how geoFluxus can work for you, book a demo today.

FAQs

What is the current CSRD effective date?

CSRD reporting starts in 2025 for former NFRD companies, in 2028 for large EU companies under the revised 1,000-employee scope, and in 2029 for qualifying non-EU groups, while listed SMEs are expected to fall out of mandatory scope altogether.

Do CSRD delays mean we can postpone preparation?

No. Most CSRD preparation work relates to data collection, governance and systems, which take time regardless of formal deadlines.

Does CSRD apply to non-EU companies?

Yes. Large non-EU companies with significant EU turnover and at least one EU subsidiary or branch fall under the CSRD timeline for non-EU companies and will need to begin reporting in 2029.

When does assurance become mandatory?

Limited assurance applies initially, with a move towards reasonable assurance planned over time.

What data causes the biggest CSRD challenges?

Non-financial information such as waste, materials, value chain impacts and environmental performance is typically the hardest to standardise and verify.